April 30-Day Money Saving Challenge

Another month is about to start. This year, we all have to admit things are a little different than normal. But, that’s OK we’ll get through it. For the month …

Another month is about to start. This year, we all have to admit things are a little different than normal. But, that’s OK we’ll get through it. For the month …

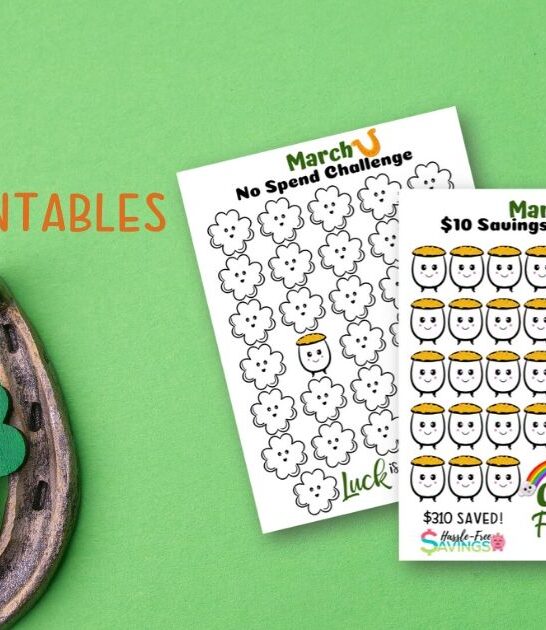

For your saving pleasure, I’d like to introduce 3 free printable saving charts. This month I am keeping things super simple with a Saint Patricks Day theme. I’ve been playing …

February is just around the corner. It marks an interesting time for most budgeters. You see, so many of us set resolutions and goals for the New Year. In January, …

Nobody wants to be in debt. However, if it were easy to repay debt, people wouldn’t need to worry about this issue. It’s a fact that getting into debt is …

Creating a budget doesn’t have to be time-consuming or difficult. In reality, the simplest budgeting strategies are typically the most effective. You can securely prevent overspending and steadily grow your …

Now that summer is here, parents all over can finally get their kids away from the TV and video games and into the great outdoors, where they may run about …

Even though going out to dinner with friends is a lot of fun, doing nothing else together might grow monotonous after a certain point, not to mention the fact that …

Checking our bank account during payday can be both exciting and overwhelming. We start to imagine all the stuff we can finally check out of our online shopping cart. Suddenly, …

In 2022, the US inflation rate rose to an all-time high in 40 years. Since then, the high inflation rate has led to increased prices in almost everything, thus decreasing …

Moving to a new state is fun and refreshing until you have to pay for all the expenses that come with the move. Fortunately, with prior planning, you will be …

People wear jewelry for varying reasons. You can wear them for identification, personal status, beauty, or to signify an event. Whatever the function, jewelry is often an investment. It can …

After an intense week of work, school, or both, you deserve nothing but fun throughout the weekend. However, you don’t have to spend too much to have fun. How can …

Hello December, Good Bye 2022! Money saving challenges and December are kind of like oxy morons. Let’s face it, most of us are going to spend more than usual this …

Just like that November is here and most of us will now start preparing for the holiday season. No doubt this year will be different than most but we can …